Not long ago, BPCE, the fourth largest bank in France, succeeded in the success of Fidor, a traditional German banking subversive. Earlier this quarter, there were two similar transactions in the world - Ant Financial was considering buying a 25% stake in the German bank software company Wirecard, while Germany's Fintech incubator FinLeap launched the new solarisBank.

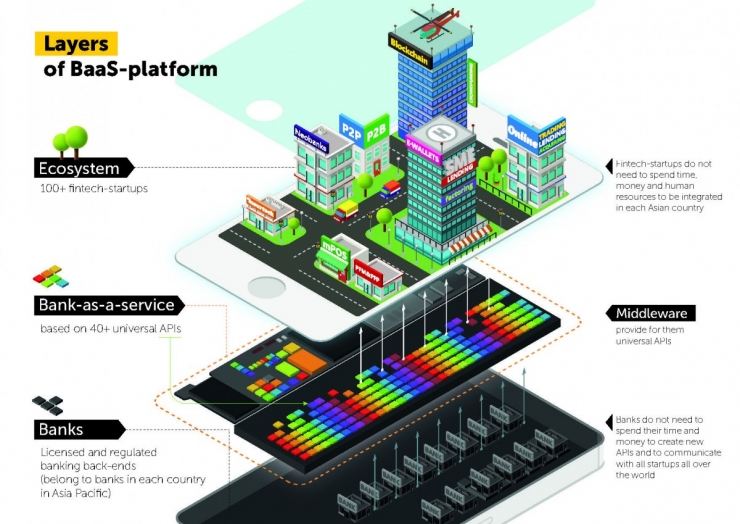

What are the commonalities between the above messages? Forbes magazine reported that, apart from that, the three major companies are developing the BaaS platform - Bank-as-a-service, leasing banking infrastructure for other participants (including licensing, payment, etc.) Processing, bank card issuance and compliance) so that they do not need to develop or purchase. This is a very new phenomenon, and with the interest of Fintech startup companies, this phenomenon is becoming more and more common.

For start-ups, they have their own bank permits (and this is not the focus of their attention) at the beginning of the business. The costs are too high. At the same time, they need new licenses and infrastructure to expand overseas. Negotiating and integrating with cooperative banks takes too much time, effort and money. As for the traditional banks that have their own core business and kpi, they do not have a clear strategy and skills to quickly and cost-effectively interface with Fintech startups. It is worth mentioning that not only Fintech startups have created demand for emerging industries: Telecom and e-commerce giants are also interested in such middleware platforms.

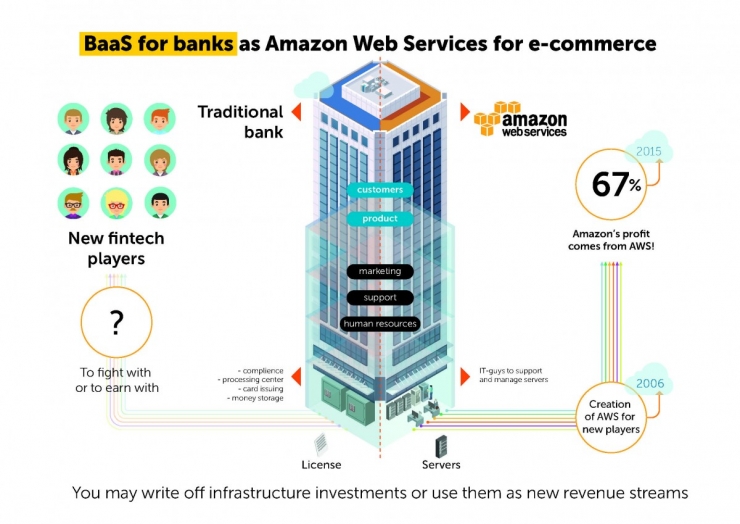

Let's look at another interesting fact: At the end of April, Amazon’s financial report showed that the cloud service AWS achieved a record revenue and profits accounted for 67% of Amazon’s total profit. Why did the incident cause interest in banks and financial technology companies? Amazon CEO Bezos has invested millions of dollars to build an excellent infrastructure to support and expand Amazon's business. At the same time, many new service providers, including new e-commerce companies, emerged in the market and competed with them. They watched them build their own infrastructure, and they expected that they would eventually run out of time and then fail - that would be better Cooperation - He decided to rent out his own infrastructure services to these new service providers.

Similar to the bank, Bezos did not use other online services as competitors or enemies, but decided to become their best partner and make profits from it. The fact is: If a startup company wants to build its own infrastructure, it must pay a cost. If you lease it out, you need to invest resources, but you will get a new source of income. At present, AWS says it wants to transform from cloud storage to "Internet's operating system."

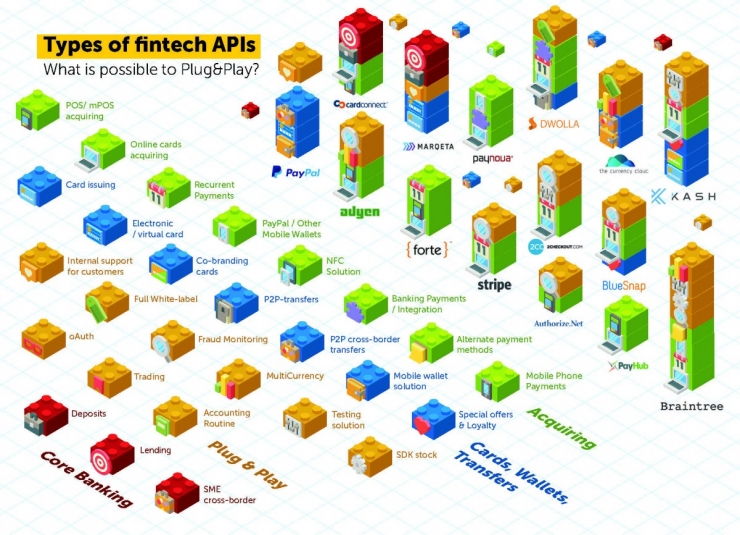

By connecting the BaaS platform, banks can lease their infrastructure to Fintech startups. For start-up companies, this will greatly reduce their costs, and accelerate and simplify the company's operations and scale development process. For banks, this creates new profit growth points for them and expands their product lines. Currently, giants such as PayPal and Stripe have begun to expand their product offerings through third-party developers. Third-party developers provide open APIs to process their services and integrate them into external applications.

The original author used to invest in financial technology in Europe and the United States. He said that he visited most banks and Fintech startups in Asia in the past year and found that no bank can successfully create its open API or have a clear understanding of new services. The agenda. Therefore, this has led many startups to spend more than a year and more than 80% of their resources to prepare for the official opening. However, taking a counterexample, when their US competitors prepare for the establishment of the company, they can spend 80% of resources on Hey Bank's BaaS platform for product development, customer acquisition and service.

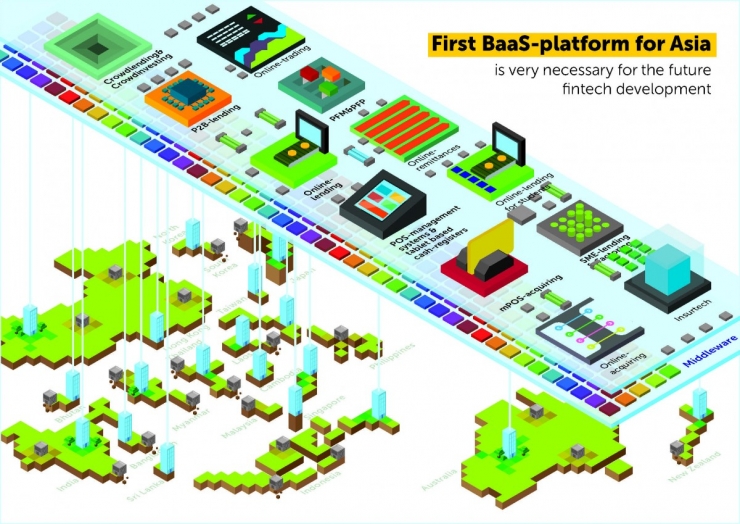

Another view is that the BaaS platform should be truly independent and cover the entire Asia Pacific region. The essence of the digital world is that you must continue to expand into new markets; if you want to take root in a country, you also need to carry out traditional offline business. The startup must seek new banks and enter into each new market through its integration with it. However, they do not want to look at the "emotions" of cooperating banks to do things, and they can be integrated into every national market from the very beginning. On the contrary, once they are merged with the platform, they can start online service faster and cheaper, and at the same time expand to new markets without barriers.

This is particularly important for the market without bank accounts - Myanmar, Laos, Cambodia, Vietnam, etc. From the accessibility of Fintech startups to the market, such platforms can reduce their gaps and gaps with developed countries. Otherwise, when companies continue to expand overseas, these countries and people will be even more isolated from the latest financial technology.

Finally, we should ask banks, especially Asian banks, that they hope to rely on the support of the regulators - and continue to protect their own local markets by isolating new competitors. Still willing to earn 67% of profits through leasing business like Amazon?

Tubular Motors with DC power supply.

Dc Tubular Motors,Constant Speed Tubular Motor,Electronic Limit Tubular Motor,Mechanical Limits Tubular Motor

GUANGDONG A-OK TECHNOLOGY GRAND DEVELOPMENT CO.,LTD. , https://www.a-okmotor.com